It is no surprise to anyone that older people are more vulnerable. But their vulnerability doesn’t just involve their health, but also their finances. The poverty incidence among senior citizens (above 60 years old) increases with their age[1].

Not only that, but there is also an increase in the dependency ratio as older people need help from their families to take care of their needs in terms of specific elderly care.

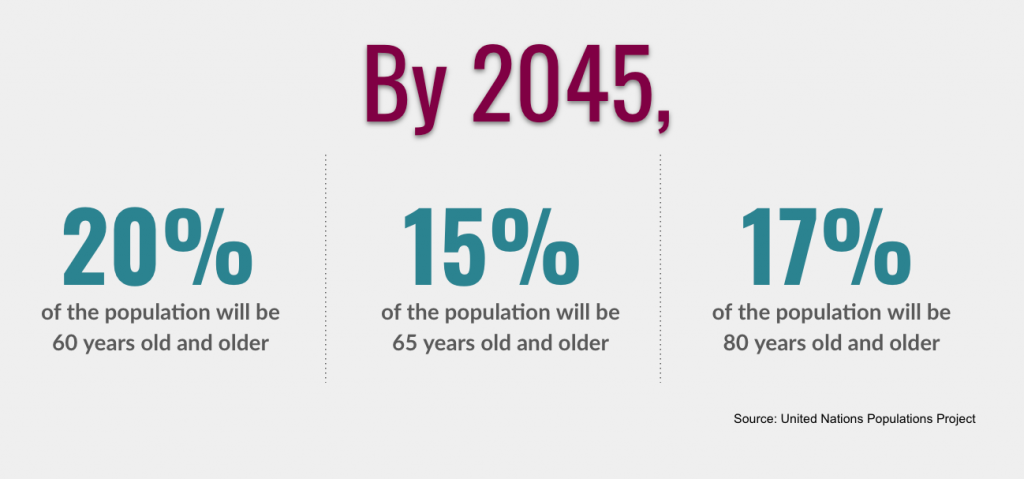

According to the United Nations Populations Project, Malaysia will be an aged nation by the year 2045[2] and “super-aged” nation by 2060 [3].

What do the increasing number of senior citizens mean?

Heads of households who are elderly (above 60 years old) are particularly vulnerable. They are over-represented at a whopping 60.5% of the B40 population[4].

The state with the highest number of low-income senior citizens is Perak, followed by Penang, Melaka, Perlis and Kedah. However, things will look pretty different by 2040 where Penang is predicted to have the highest number of low-income citizens followed by Kuala Lumpur and Selangor[1].

Do All Senior Citizens Have A Retirement Fund?

Life expectancy at birth in Malaysia has increased to more than 70 years[4]. The increase of life expectancy predictably brings about challenges in the sustainability of public pensions, public healthcare funding and other social safety nets[6].

The minimum retirement age is 60, but most EPF savings are only enough to sustain a humble living for an estimated 5 years[5]. If things are so dire for pensioners, having sufficient retirement funds is even more worrying for workers in the private sector, freelancers and the self-employed[6].

The elderly are dependent on their life savings or family support, especially if they are no longer working. Financial security is always a concern, mostly if they are not covered by any social assistance programmes[7].

The Asian Filial Piety Proves Beneficial

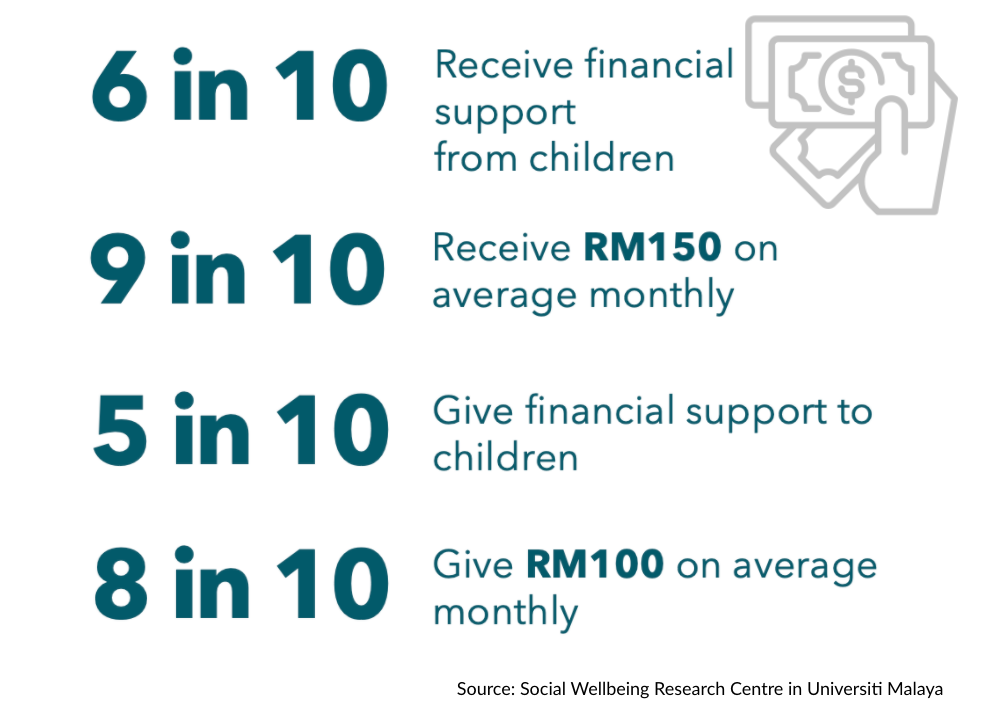

A study in January 2021 by the Social Wellbeing Research Centre in Universiti Malaya revealed a lot about the Asian culture and their family relations in relation to money and caregiving.

Family support is crucial in elderly care and does not necessarily only cover finances. It also includes non-financial support such as household items and clothing, medication, groceries, help with household chores, emotional support and more[2].

The study also found that the amount of financial support received from their children increases with age. In return, the amount of financial aid given to their children decreases with age. Of these respondents, elderly women received slightly more financial assistance than men[2].

What About Retirement Funds?

Only 60.8% of the Malaysian labour force contributes to the Employees Provident Fund (EPF)[7].

Not only is this number low, but almost 75% of these members also have less than RM250,000 in their accounts at 54 years-old. This translates to a monthly income of less than RM1,050[7]. To add to the number, less than 45% of EPF members aged 54 have savings more than RM50,000 in 2020 [3].

Can you imagine surviving only with RM1,050 a month, especially with growing health concerns and possible unexpected expenses?

Can Senior Citizens Continue to Work To Reduce The Risk Of Poverty?

There are many senior citizens who wish to continue working beyond the age of 60 years old.

43.1% of men and 50% of women aged 60-64 years old are self-employed, meaning they are either business owners or freelancers[7].

Self-employment is one way to continue generating income past retirement age, however, it is not feasible for all segments of society. Senior citizens find it hard to retain employment in the marketplace if they don’t have a specific or niche skillset that is in high demand.

Tunku Alizakri Raja Muhammad Alias, the deputy chief officer of EPF, suggested raising the retirement age from 60 years, to 65 years old instead, as many elderly are still able to work and have skills to offer in the market. For example, industries that could use their expertise and experience in coaching, consultancy, and even childcare[8].

The Covid-19 pandemic worsens the situation for senior citizens living in poverty or on the brink of it. A situation like the pandemic makes their vulnerability more evident. It drastically reduces their life savings and makes it even more difficult for them to rejoin the workforce[1].

The elderly who need to continue working would have a harder time re-entering the workforce not only because of Covid-19 business closures but also because of greater ageism as businesses may cut budgets to survive and restructure finances.

Assoc Prof Saidatulakmal, Director of USM’s Centre for Global Sustainability Studies[1].

The problem with the government pensions offered in Malaysia is that more than 30% of the population is not covered by it. But even having a pension is not a relief as most of the savings accumulated are inadequate to finance the expenses of full retirement[1] as many are receiving an amount lower than the recommended 40% of previous earnings [3].

Schemes To Help Senior Citizens

The core issue with ageing poverty is that the government’s pension schemes exclude a significant population.

The second group of seniors are not covered by those schemes. Still, they are instead assisted by a host of other social assistance programmes run by other organisations. However, even these are not enough to adequately cover an acceptable amount of the elderly population in need, much less all of them[9].

“Despite a large number of programmes, these arrangements exclude a significant share of those who are targeted,” Dr Amjad Rabi, a visiting expert at the University of Malaya’s Social Wellbeing Research Centre[9].

SOCSO

Others who are still left out of these financial aid schemes turn to other solutions, such as the invalidity pensions from SOCSO. In 2017, SOCSO had more than 14,000 applicants for invalidity pensions, but only 40% were approved[9].

BANTUAN SARA HIDUP

The Bantuan Sara Hidup Scheme is another form of government aid that the elderly have been trying to utilise. It targets lower-income groups and provides them with a one-off payment of RM1,000. In 2016, it was recorded that 28% of the recipients were elderly. This number alone corresponds to 54% of senior citizens in Malaysia[9].

BANTUAN ORANG TUA (BOT)

The Bantuan Orang Tua(BOT) scheme is handled by the Ministry of Women, Family and Community Development. This programme alone grew 4.2 times larger from the span of 2008 to 2016. In 2017, it covered a total of 133,352 elderly recipients[9].

It should also be noted that although Malaysia seems to have quite a few social welfare schemes and programmes for the elderly, they are not united under a single umbrella and are rather scattered. This could cause problems for elderlies to identify organisations which would benefit them or leave them out of the loop entirely as some fall under the radar.

The World Bank also noted that even with all this, the amount of money that the country spends on social assistance is low compared to most upper-middle-income nations[1].

Malaysia spends RM14.6 billion, only 1% of our GDP on social welfare programmes in 2018. However, other upper-income nations in the same category as Malaysia tend to spend an average of at least 1.6% of their GDP for social welfare[1].

In light of this, the World Bank proposed that the country develops a Social Protection Master Plan instead. This would shift the current norm of a varied set of social protection programmes, to instead become a proper social protection system that is unified. They also suggested that the masterplan be a document that is directly able to be put into action, rather than a study of suggested strategies and outcomes like now[10].

Other options have also been suggested to alleviate ageing poverty. These include multiple economic policies such as increasing the retirement age, making workplaces more inclusive of older folk and implementing a streamlined monthly social pension for targeted groups of elderly that is not reliant on their personal pension accounts[10].

Explore Our Sources:

- Murad, D. (2020, June 28). Providing for an ageing population. The Star. Link.

- Malaysia Ageing and Retirement Survey (MARS) Wave 1 2018/2019: Key Findings. (2021). Social Wellbeing Research Centre (SWRC). Link.

- Khazanah Research Institute. (2021). Building Resilience: Towards Inclusive Social Protection in Malaysia.

- Rabi, A., Mansor, N., Awang, H., & Kamarulzaman, N. (2019). LONGEVITY RISK AND SOCIAL OLD-AGE PROTECTION IN MALAYSIA: Situation Analysis and Options for Reform. Social Wellbeing Research Centre (SWRC). Link.

- Mazlan, M. (2015). Time to be mindful of old-age poverty. New Straits Times. Link.

- Yeap, C. (2020). Special Report: Ensuring the well-being of the old, poor, sick, childless and jobless in the coming two decades. The Edge Markets. Link.

- World Bank. (2020). A Silver Lining: Productive and Inclusive Aging for Malaysia. Link.

- Nori, A., Dr. (2017). Ageing gracefully to 2045. New Straits Times. Link.

- Bhattacharjee, R. (2020). Politics and Policy: Old and out of money. The Edge Markets. Link.

- Lim, I. (2020, June 26). Malaysia’s ageing population challenge: World Bank moots RM350 monthly govt-funded ‘social pension’ for B40 elderly as a start. Malay Mail. Link.